Fulfillment by Amazon (FBA) is the logistics model that lets sellers store inventory inside...

In this article

- What Does COGS Mean

- What Is COGS in Business

- What Is Included in COGS

- COGS Formula Explained

- How to Calculate COGS (Step-by-Step)

- Example of COGS Calculation

- COGS in E-commerce and Amazon Sellers

- FIFO vs Average Costing for E-commerce

- Why COGS Is Important for Profitability

- Common Mistakes When Calculating COGS

- How Businesses Use COGS in Decision Making

- FAQ

If you are asking what is COGS, start with the COGS formula: beginning inventory plus purchases minus ending inventory. This guide shows how to calculate COGS with examples finance teams can defend at month-end close.

Cost of goods sold is the single most important input in a gross profit calculation — yet it is regularly misunderstood, miscategorized, or tracked with costing methods that distort margins at scale. This guide covers what COGS means, what it includes, how to calculate it with a worked example, which costing method produces accurate results as your catalog grows, and how to use it as a decision-making tool across pricing, procurement, and financial planning.

What Does COGS Mean

COGS is one of the most important financial metrics in business accounting because it directly determines how profitable a product or service actually is. In simple terms, it reflects the direct costs required to produce or purchase the goods that a company sells during a specific period.

The COGS meaning in business refers to all direct costs tied to production or acquisition of products, excluding indirect expenses such as marketing or administrative overhead. This distinction is essential because it separates what it truly costs to deliver a product from what it costs to run the business as a whole.

From an accounting perspective, COGS is used to calculate gross profit. It helps businesses understand whether their core operations are financially sustainable before considering additional expenses like advertising or salaries.

In financial reporting, COGS is consistently tied to profitability analysis. Investors and managers use it to evaluate efficiency, pricing strategy, and cost control.

What Is COGS in Business

Understanding COGS in business is essential for any entrepreneur or financial analyst. It represents the direct relationship between revenue and production cost.

In practice, it refers to how much it costs a company to deliver its product to the point of sale. If a business sells physical goods, COGS includes manufacturing or purchase costs. If it sells services, COGS includes labor directly tied to service delivery.

More broadly, COGS is the foundational metric that determines gross profitability. Without accurately tracking it, businesses risk mispricing products or misjudging their margins — leading to cash flow problems even in high-revenue operations.

What Is Included in COGS

To correctly understand COGS, it is important to separate direct production-related costs from indirect business expenses. Only costs directly tied to producing or acquiring goods for sale are included. Everything else — marketing, administration, office operations — is excluded.

This distinction is critical because it directly affects gross profit calculation and determines how efficiently a business turns inventory into revenue.

| Cost Category | Included in COGS | Not Included | Explanation |

|---|---|---|---|

| Raw materials | Yes | No | Direct inputs used to create the product |

| Wholesale product cost | Yes | No | Cost of buying finished goods for resale |

| Manufacturing labor | Yes | No | Direct labor involved in production |

| Packaging materials | Yes (if product-related) | No | Packaging required to sell or ship the product |

| Inbound shipping | Yes | No | Shipping goods to warehouse or fulfillment center |

| Storage fees | Sometimes | No | Included only if directly tied to inventory handling |

| Advertising & marketing | No | Yes | Considered an operating expense, not a production cost |

| Office rent | No | Yes | Indirect overhead cost |

| Salaries (admin staff) | No | Yes | Not directly tied to production |

Understanding what is included in COGS is essential for accurate financial reporting and decision-making. Businesses that incorrectly classify expenses risk overstating or understating profitability. If non-production expenses are mistakenly included, profit margins may appear lower than they actually are.

For e-commerce businesses and Amazon sellers, this classification becomes even more important because product-level profitability depends on precise cost tracking. For a detailed comparison of COGS and landed cost — two metrics that are closely related but serve different analytical purposes — see COGS vs Landed Cost.

COGS Formula Explained

The standard COGS calculation formula is:

COGS = Beginning Inventory + Purchases − Ending Inventory

This formula tracks how much inventory was used during a period and converts it into a monetary cost.

It is important to understand that COGS is not simply the cost of buying products. It is adjusted for inventory changes, which makes it a dynamic accounting measure rather than a fixed expense. A business that purchased $50,000 in product but still holds $20,000 of it unsold has a COGS that reflects only what actually moved through the sales process.

How to Calculate COGS (Step-by-Step)

To accurately calculate COGS, businesses need to follow a structured inventory-based approach rather than simply summing purchase costs. COGS is not a static expense — it reflects how inventory moves through the business over a specific accounting period.

The calculation connects what a company had at the beginning, what it purchased during the period, and what remained unsold at the end. This structure ensures that only the cost of actually sold goods is included in financial reporting.

- Determine Beginning Inventory. Identify the value of inventory available at the start of the accounting period. This represents all products that were not sold in the previous cycle and are carried forward into the current period. Beginning inventory is important because it forms the baseline of the calculation — without it, businesses would underestimate the true cost of goods sold, especially if they maintain stock across multiple periods.

- Add New Purchases or Production Costs. Add all additional costs incurred during the period. This includes not only new inventory purchases but also any direct costs required to make products ready for sale: wholesale product purchases, raw materials, manufacturing expenses, product-related packaging, and inbound shipping to warehouses or fulfillment centers.

- Subtract Ending Inventory. At the end of the accounting period, determine the value of unsold inventory. Subtracting this amount is essential because it removes products that were not actually sold. Only inventory that moved through the sales process should remain in the final COGS figure.

- Verify Unit Costs. Confirm that all unit costs are accurate and consistent across the entire period. This involves checking whether product costs remained stable or changed due to supplier pricing shifts, freight fluctuations, or currency exchange rates.

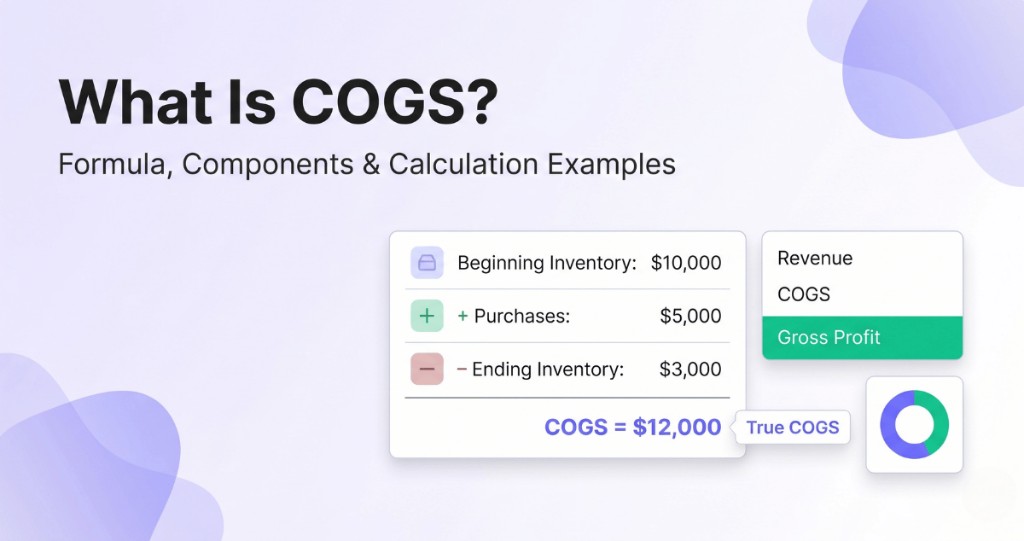

Example of COGS Calculation

To illustrate the process, consider a straightforward scenario:

Beginning Inventory: $10,000

+ Purchases during the month: $5,000

− Ending Inventory (unsold): $3,000

COGS = $10,000 + $5,000 − $3,000 = $12,000

This means the company's cost of goods sold for that period is $12,000. The remaining $3,000 in inventory carries forward to the next period as beginning inventory, ensuring continuity in the calculation cycle.

COGS in E-commerce and Amazon Sellers

For online businesses, especially sellers on Amazon, COGS plays a central role in determining product profitability.

In e-commerce, COGS typically includes product cost, shipping from supplier, packaging, and fulfillment-related costs. Sellers rely on accurate COGS tracking to set prices, evaluate margins, and scale their product catalog effectively.

Without precise COGS calculation, sellers risk underpricing products or misjudging profitability, which can lead to cash flow problems even in high-revenue stores.

For a deeper practitioner guide specific to Amazon sellers — covering settlement fee reconciliation, FBA cost structures, and marketplace-level adjustments — see Amazon COGS Formula: Practical Guide for Accurate Calculations. This article is the conceptual primer; that one goes further into the mechanics of Amazon-specific cost allocation.

FIFO vs Average Costing for E-commerce

Two inventory costing methods determine how COGS is calculated at the unit level: average costing and FIFO (First-In, First-Out).

Average costing blends all purchase costs into a single weighted average per unit across all batches. For a simple catalog with a single supplier and stable pricing, this produces an acceptable approximation. As a business scales — multiple purchase orders at different prices, international sourcing, carrier rate fluctuations, FBA shipments arriving at different duty rates — the blended average drifts further from actual per-batch economics.

Consider a concrete example. You receive 500 units at $8.00 in January and 500 more at $11.00 in March due to a freight rate increase. Your weighted average cost becomes $9.50 per unit. In April, you sell 400 units — all drawn from the January batch. Your actual COGS is $8.00 × 400 = $3,200. Average costing reports $9.50 × 400 = $3,800. The $600 gap is phantom COGS: it overstates your cost, understates your gross margin, and delivers the wrong signal to pricing and forecasting teams.

FIFO eliminates this distortion. It tracks which specific batch was consumed — the oldest receipt is depleted first — and assigns that batch's cost to the units sold. The result is per-unit COGS that reflects actual purchase economics, not a statistical blend. When unit costs vary significantly between batches, FIFO is the only method that produces defensible margins.

NeonPanel's batch-level FIFO COGS engine allocates landed costs — freight, customs duty, 3PL prep fees — to each receipt batch at the shipment level and tracks consumption in true FIFO order. Gross margin calculations reflect what was actually paid for the units that actually sold, not what the average suggests. For e-commerce brands sourcing internationally or managing FBA shipments at different cost points, this is the layer that makes reported margins trustworthy.

See how it works: Landed Cost & FIFO COGS and Automatic COGS. For more on what landed cost includes and how it flows into COGS, see What Landed Cost Is and Why It Matters and Full Landed Cost Explained.

Why COGS Is Important for Profitability

COGS directly impacts gross profit, which is one of the most important indicators of business health. Without accurate COGS tracking, businesses cannot correctly evaluate pricing strategy or product viability.

It also helps identify underperforming products, optimize supplier negotiations, and improve cost structure over time. In many cases, small changes in COGS can significantly affect overall profitability.

From a financial planning perspective, accurate COGS allows companies to predict margins with confidence and adjust strategy before losses appear — rather than discovering cost overruns at month-end close or during due diligence.

Common Mistakes When Calculating COGS

Many businesses encounter the same recurring accuracy gaps in COGS calculation:

- Excluding inbound shipping or packaging costs from product-level unit cost

- Classifying marketing or advertising expenses as COGS

- Failing to track inventory changes accurately across periods

- Using outdated unit costs that no longer reflect current supplier pricing

- Ignoring price fluctuations between purchase orders

These errors distort financial analysis and lead to incorrect decisions on pricing, product selection, and margin forecasting.

How Businesses Use COGS in Decision Making

COGS is not just an accounting metric — it is a strategic instrument.

Businesses use it for pricing optimization, product selection, and profitability forecasting. It also plays a key role in negotiating supplier contracts and managing inventory levels. A product with high revenue but a COGS that consumes most of that revenue is worth far less than it appears in top-line reporting.

In financial planning, understanding COGS allows companies to predict margins more accurately and adjust strategy before losses occur. Businesses often analyze the COGS percentage — the share of revenue consumed by direct production costs — to benchmark performance across products or categories and identify where cost reduction efforts will have the greatest impact.

For e-commerce operations running across Amazon, Shopify, and other channels, COGS accuracy becomes a coordination problem as much as an accounting one. When costs are tracked at the channel level and reconciled against actual inventory consumption, the resulting margin data is reliable enough to drive decisions at every level of the organization. NeonPanel's ecommerce accounting platform is built for exactly this use case.

Ready to see your real COGS — batch by batch, channel by channel?

NeonPanel allocates landed costs to every receipt batch, tracks consumption in true FIFO order, and posts accurate COGS directly to QuickBooks or Xero — across Amazon, Shopify, and every other channel. See how FIFO COGS works in NeonPanel →

Further reading: Amazon COGS Formula: Practical Guide · COGS vs Landed Cost · Fully Landed Cost Explained

FAQ

What does COGS stand for in finance and business?

COGS stands for Cost of Goods Sold in finance and business. It represents the direct costs associated with producing or purchasing the goods a company sells, and it is a key metric for calculating gross profit.

What is COGS in business?

COGS in business refers to the total direct expenses required to produce or acquire products sold during a specific period. It includes materials, manufacturing costs, and purchase expenses, but excludes indirect costs like marketing or administration.

What is COGS in accounting?

In accounting, COGS is used to measure the cost of inventory that has been sold during a reporting period. It is a core part of financial statements because it directly impacts gross profit calculation and overall business performance.

What are COGS in business?

COGS in business are the direct costs tied to product creation or acquisition. These typically include raw materials, production labor, wholesale purchase costs, and inbound shipping expenses related to inventory.

How to find COGS?

To determine COGS, a business tracks beginning inventory, adds new purchases or production costs, and subtracts ending inventory. This method ensures that only the cost of goods actually sold is included in the final calculation.